1. Introduction

The Challenge of Stock Picking

If, on November 1, 2022, your portfolio consisted entirely of Nvidia [NVDA] and no other stocks, well done you. Two years later, its value would have increased by slightly over 900%; in other words, a 10-fold increase.

Chances are, though, that very few portfolios consisted of just Nvidia at this time, and for good reason: the stock’s breathtaking rise was — at least before the launch of ChatGPT at the end of November 2022 — very hard to predict.

This is true of all individual stocks, at all times. Stock picking is a notoriously difficult game, even for professionals. As Burton Malkiel wrote in A Random Walk Down Wall Street, “a blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts.”1

The challenge is compounded by the fact that, over the long term, very few stocks actually generate meaningful returns. A 2018 paper by Arizona State University Professor Hendrik Bessembinder entitled Do stocks outperform Treasury bills? showed that the entirety of the $35trn in wealth created by the stock market from 1926–2016 was derived from just 1,092 stocks — a little over 4% of the total2. The total returns of the remaining companies — almost 96% — generated the same return that investors would have realized through investing in Treasuries.

The Risk-Reward Dilemma

There are several reasons for this. One is that, as Bessembinder identified, stocks have a surprisingly short average lifetime.

“The median time that a stock is listed on the CRSP database between 1926 and 2016 is seven-and-a-half years,” he wrote. This, naturally, reduces the average timeframe that stocks have to make gains, and underscores the fact that many of them, ultimately, go to zero.

Which leads onto a bigger issue: stocks are volatile. While many will enjoy periods of gains, what goes up often comes back down again. Because of a quirk of mathematics, this has serious implications for long-term investors.

A portfolio that is worth $100,000 and gains 50% will then be worth $150,000. However, if it then falls 50%, it will not equal its starting value; it will in fact be worth $75,000, or 25% less than its starting value.

Similarly, if a $100,000 portfolio falls by 50%, it will be worth $50,000. A subsequent 50% increase will only recoup half of these losses: it takes a 100% gain to reverse a 50% loss.

In short, falls in share prices hurt a portfolio far more than gains benefit them.

This is not to mention the well-worn truism that ‘markets go up in escalators but down in elevators’3. Stock market gains tend to take place gradually, over months, years or even decades. When investor sentiment turns, however, their value descends rapidly, often in days or even hours.

The upshot is that, at least as much as it is about picking winners, long-term investing is about avoiding losers. Fundamentally, investors have to take risks in order to generate returns. The higher the risk, the higher the potential return, and the higher the potential losses4.

Investors frequently fall foul of this basic law; the desire to concentrate portfolios in a small number of stocks or sectors that can generate high returns over the short run often hampers their long-term performance.

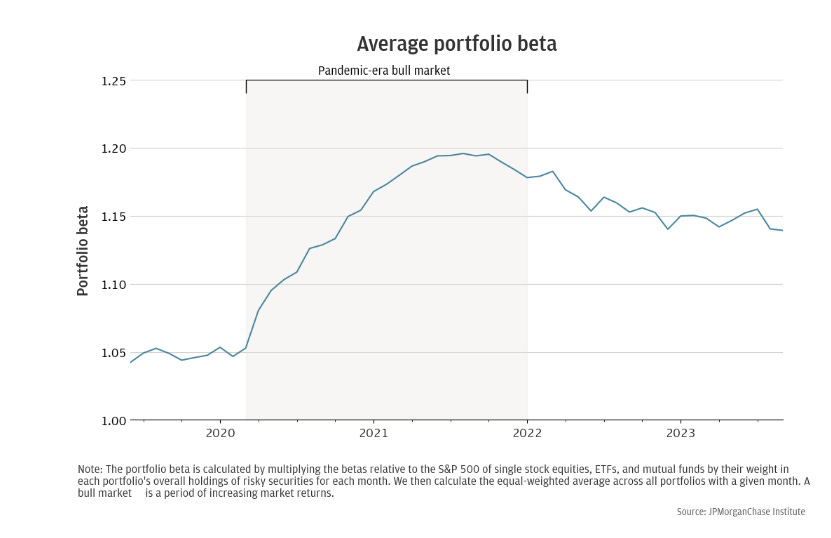

Downside risk management is, therefore, at least as important for investors as the ability to pick high-performing stocks. However, retail investors are notoriously poor at managing their risk levels. Research from the JPMorganChase Institute found that the amount of risk in retail investor portfolios increased substantially during the Covid-19 pandemic, and remained elevated through 20235.

Much of the reason for this is emotional. For example, investors can succumb to FOMO when a stock or sector is experiencing a bull run, leading them into performance chasing or going all-in during a period of high returns6. Unconscious biases can creep in; men, for example, tend to hold more risk in their portfolios than women, according to JPMorganChase.

In order to overcome these unconscious biases and emotional influences, investors need a portfolio management strategy7. This is a means of selecting and rebalancing portfolio constituents in order to match it to the investor’s long-term financial objectives and risk tolerance levels.

While there are various types of portfolio management strategies, at their core all boil down to a set of approaches, rules or processes that govern which stocks are added to or sold from the portfolio, and when, in order to effectively balance risk and reward.

2. The Pitfalls of Individual Stock Picking

Market Complexity

No one can predict with accuracy how share prices will move in future — not even the Wall Street analysts whose job it is to research stocks and markets in the most minute detail.

A study published in the International Review of Economics and Finance published in June 2024 found that analyst price target forecasts “tend to commit systematically upward bias (9.4%), large absolute pricing error (24.8%), over-prediction of the actual price changes (21%), and a low proportion (54%) of correct directional forecasts”8. That last point is worth reiterating; more than half the time, analysts were wrong about whether a stock would go up or down.

That study focused on analyst targets in Taiwan, an emerging market, but the bulk of scientific study that has been carried out tends towards the same conclusion: not even stock market analysts are good predictors of future share price movements9.

The reason for this is simple: markets are volatile and highly complex, and share price movements are impacted by an impossibly large number of factors, most of which are themselves impossible to predict in advance.

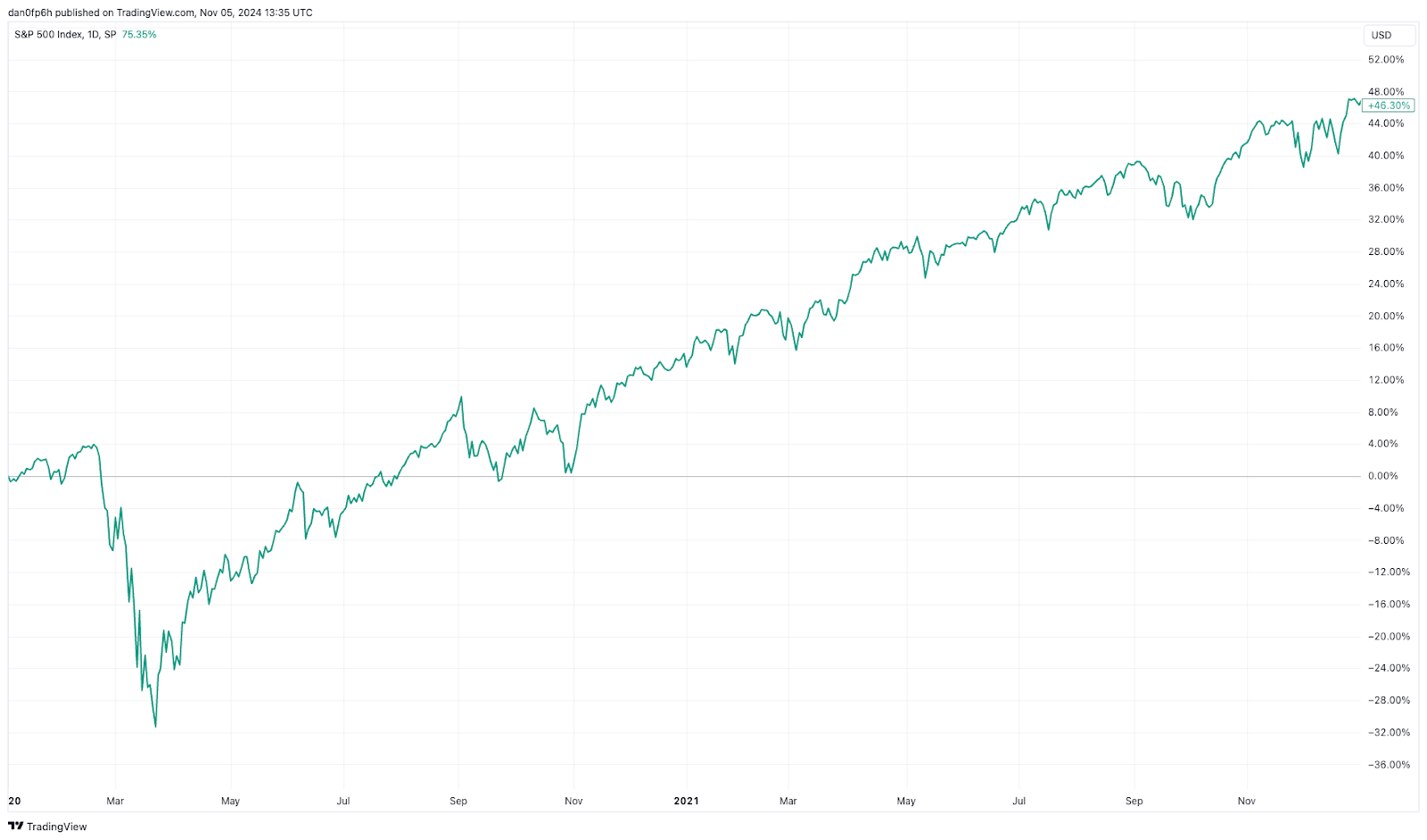

The pandemic provides a neat example of this. The chart below shows the S&P 500 between the start of 2020 and the end of 2021.

The index nosedived in March 2020 as the pandemic forced the US into lockdown. Investors sold their stocks rapidly, in the (not unreasonable) expectation that this lockdown would hurt the economy and that this would have a knock-on effect on the value of their shares.

By August, however, the index had recovered to its February levels, and through the remainder of 2020 and the entirety of 2021 it entered a strong bull run, prompted by the exact same pandemic that triggered its crash in the first place.

As easy as it is to say, retrospectively, “of course Zoom [ZM] and Moderna [MRNA] were going to be big winners from the pandemic”, investors in March 2020 could not have known it. Even if they suspected that these kinds of stocks might do well out of an extended lockdown, it would have been hard to predict which stocks in particular would be the big winners.

There is another very important lesson in the pandemic experience, though.

Roll the tape forward to November 2024, and the picture looks very different once again.

The flat, steady green line representing the S&P 500 lags behind Moderna, but the latter’s bull run is clearly over. It has still returned 178% since the start of the pandemic, but any investor that has bought and held the stock since the second half of 2020 has made a loss in the meantime, despite the huge gains it registered through 2021. Unless something unexpected (ergo, unpredictable) happens to change its course, its current trajectory looks set to fall below the S&P 500’s four-year returns within months.

Zoom, meanwhile, looked set to outperform both Moderna and the S&P 500 as of October 2020 — but, as of November 2024, it is just 9.92% up since the start of 2020. During this period, it has significantly trailed the S&P 500.

The lesson here is that all manner of stocks can have their moment in the sun when market conditions suit them. Over the long term, however, most tend to underperform against key benchmarks, such as diversified indices like the S&P 500. Investors who bought Zoom or Moderna early in 2020 will only have seen a return if they sold some of their holdings during their respective bull runs.

The vast majority of stocks — almost 96% — also underperform Treasury returns over the long term10. Any given portfolio therefore needs two things in order to generate meaningful returns over the long term:

Diversification. Exposure to a variety of asset classes, sectors and/or themes, and a variety of stocks within those themes, helps to ensure that the winners from any given set of market conditions are represented within a portfolio.

A mechanism to capture profits. If we accept that any given stock is likely to be a loser over the long term, strategic portfolio management has to bank the returns of any winning streak before a reversal comes about.

Emotional Decision-Making

Without a structured investment strategy, rational investing is impossible, because emotions cloud investor judgment11. Fear led investors to sell their stocks off early in the pandemic, despite the fact those shares would go on to post significant gains. Often, investors experience success with a small number of fortunate stock picks that post strong returns; this, in turn, can breed over-confidence, if the investor overlooks the extent to which they got lucky with those picks.

Herd mentality is a constant peril in the stock market. Over-exuberance tends to lead every bull run to a point at which the entire stock market is overvalued; the subsequent market contraction is often characterized by widespread fear of loss, prompting rapid selling behavior not unlike a bank run, with investors racing against each other to extract their capital from the market before it disappears12.

Similarly, there are numerous biases that naturally impact human approaches to decision-making, particularly investing. These include confirmation bias, which makes investors more receptive to information that confirms their prior beliefs; experiential bias, whereby they are more greatly influenced by experiences that happened recently; loss aversion, a disproportionate fear of loss relative to desire for gain; and familiarity bias, which skews investor interest towards areas they know over those that they do not.

Some of these biases can be beneficial — Warren Buffett is, for example, an outspoken advocate of familiarity bias13 — and because it takes a 100% gain to correct a 50% loss, a degree of risk aversion is rational. The point about all of them, though, is that they distort decision-making, usually in ways that investors are not consciously aware of.

Benefits of a Structured Approach

Developing a structured portfolio management strategy will invite investors to consider their own long-term goals. This is a major step in its own right that many retail investors overlook: the UK's Financial Conduct Authority found that just 2% of investors have a timeframe of more than five years in mind when investing, and 14% have no specific time horizon in mind at all14.

Taking this basic starting point then enables investors to consider their risk tolerance levels, and the assets they will allocate their capital towards in order to complement this15. They can then diversify strategically within these asset classes. Investing then becomes less about chancing upon an individual stock that will gain, and more about deciding which stocks can perform what function within a diversified, balanced portfolio.

Finally, a rebalancing strategy enables a strategic, systematic approach to profit-taking that does not rely on gut feel.

Read Part 2 & 3:

Part 2: The Power of Diversification

Part 3: A Holistic Approach: Diversification & Smart Allocation

This is for informational purposes only. OPTO Markets LLC does not recommend any specific securities or investment strategies. Investing involves risk and investments may lose value, including the loss of principal. Past performance does not guarantee future results.

https://www.forbes.com/sites/rickferri/2012/12/20/any-monkey-can-beat-the-market/

https://www.sciencedirect.com/science/article/abs/pii/S0304405X18301521

https://www.cdspi.com/learn/advice-for-riding-the-stock-market/

https://www.investopedia.com/terms/r/riskreturntradeoff.asp

https://www.jpmorganchase.com/institute/all-topics/financial-health-wealth-creation/retail-risk-investors-portfolios-during-the-pandemic

https://financialpost.com/investing/emotion-can-cause-investors-lose-capital

https://www.investopedia.com/terms/p/portfoliomanagement.asp

https://www.sciencedirect.com/science/article/abs/pii/S1059056024000960

https://www.danerwealth.com/blog/the-terrible-track-record-of-wall-street-forecasts

https://www.sciencedirect.com/science/article/abs/pii/S0304405X18301521

https://www.investopedia.com/terms/b/behavioralfinance.asp

https://www.linqto.com/blog/market-cycles/

https://www.investopedia.com/financial-edge/0210/rules-that-warren-buffett-lives-by.aspx

https://www.fca.org.uk/news/press-releases/young-investors-more-likely-have-long-term-goals-mind-dating-when-investing

https://www.fidelity.com/viewpoints/investing-ideas/guide-to-diversification